Performance Review

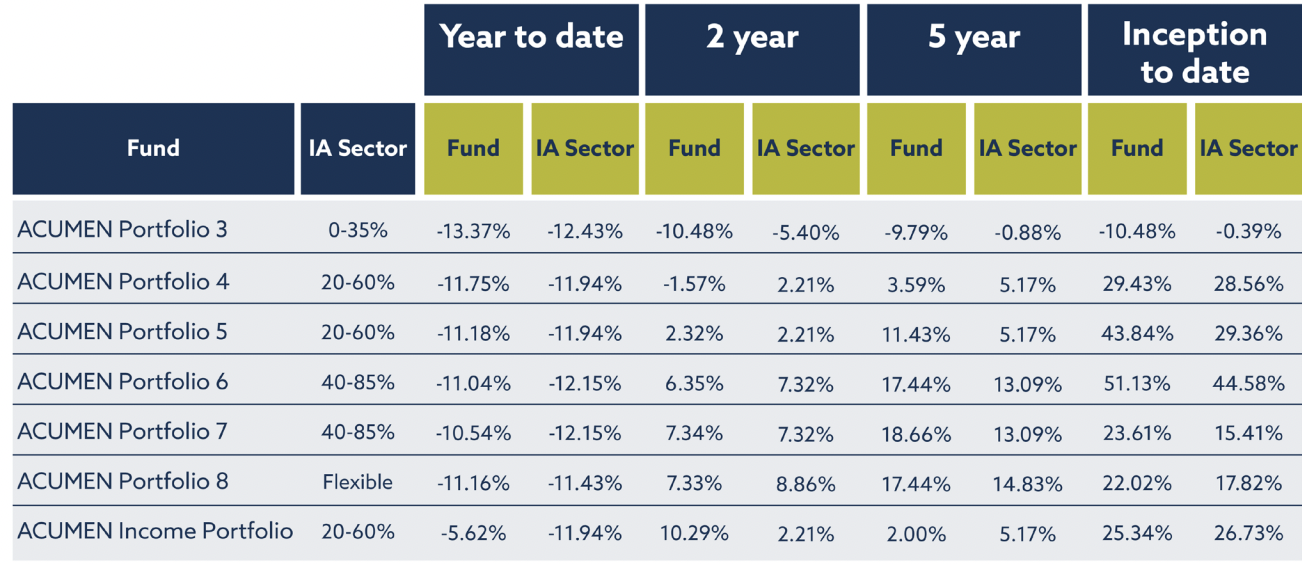

On an absolute basis the ACUMEN Portfolios have fallen in value since the start of the year. This is unsurprising given recent developments. However, on a relative basis the funds have held up well, particularly at the higher end of the risk spectrum and in the ACUMEN Income Portfolio versus the IA sector peer group against which we measure performance. On a 5-year basis, and since inception, the funds continue to perform well on both an absolute and relative basis.

Key Themes

Naturally the fall in portfolio values this year is not a desirable outcome. That said, it is consistent with market pricing, and we remain focused on the ongoing development of the proposition, adapting as required to the ever-evolving investment climate. Given the longer-term nature of the funds, it is important to flag that these periods create fantastic longer-term opportunities, and we aim to take advantage of these over time. In my ongoing conversations with advisers and clients we are mindful of the fact that as important as it is to focus on the return-on-capital over the long run, return-of-capital remains at the forefront of people’s minds, which is consistent with our more defensive outlook at this time. At this juncture it makes sense to briefly touch upon why markets have sold off and our current market outlook. We are focused on four key factors:

- the risk of global recession

- the future evolution of inflation

- scope for a decline in corporate earnings, and

- squeezed liquidity even as valuations remain relatively expensive

These factors point towards the need for caution and we have taken some initial steps to tactically raise cash and reduce risk across the proposition for this reason. The relief rally over the last month and a half should provide some near-term comfort. This was predicated on a short-term reversion of some of the above-mentioned factors. Namely, (1) third-quarter US GDP came in better than expected, bucking the prior trend of two-quarters of negative growth, (2) an article in the Wall Street Journal from Nick Timiraos (largely regarded as part of the Fed’s communication strategy) highlighted the potential for a reduction in the pace of monetary tightening as inflation starts to moderate, and (3) better than expected corporate earnings, primarily driven by the energy sector (other sectors fared far worse including US tech and comms, as evidenced by the recent decline in the Meta share price). In addition there have been growing rumours that China may pivot from its zero-covid policy, which would be a huge boost to the global economy.

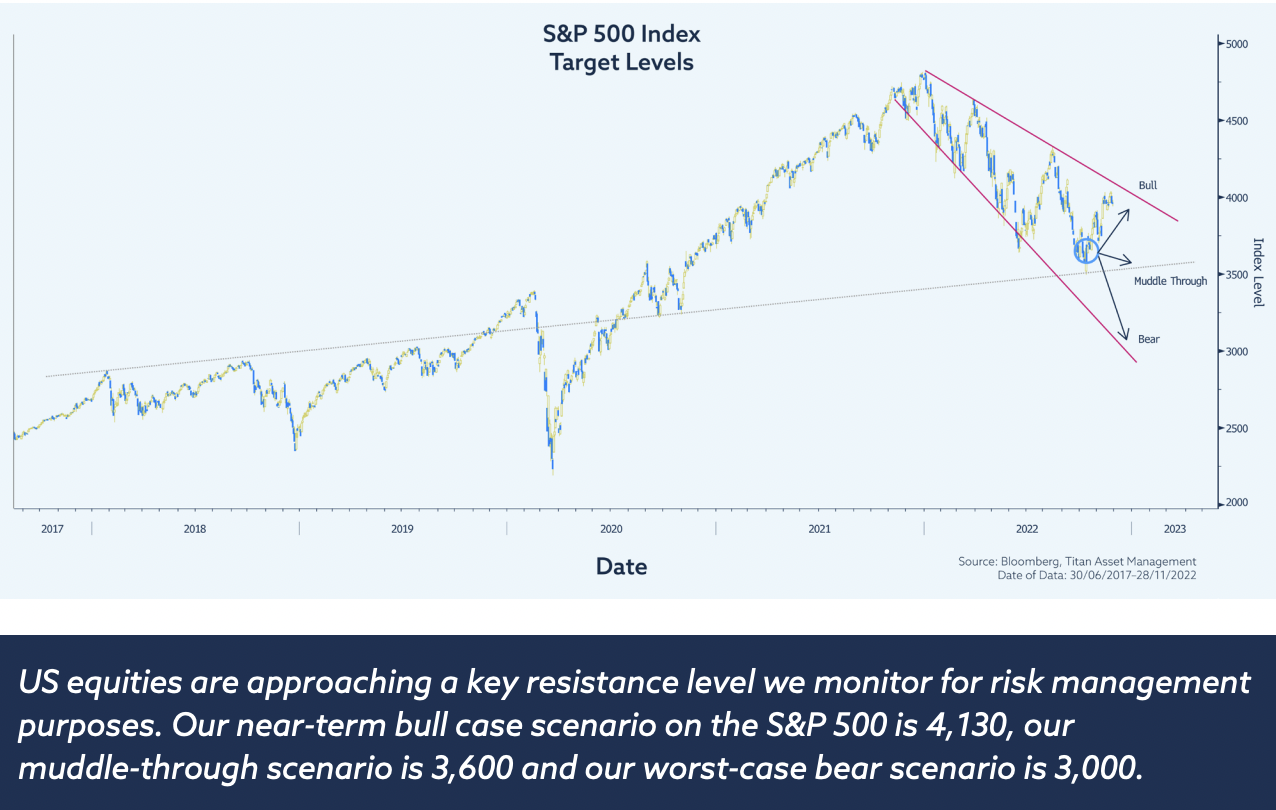

As a result, we have closely tracked the ‘bull’ case scenario we set in early October, with the S&P 500 approaching the psychologically relevant 4,000 level. Some investors I’ve spoken to believe the recent rally represents a new bull market. Whilst we can’t discount the probability of a Santa rally into year-end, we believe it is too early to make that call given the magnitude of the relief rally is consistent with other bear markets and the index is yet to break out from its current downtrend, shown in pink. Until we see evidence to the contrary, we continue to adopt a cautionary approach.

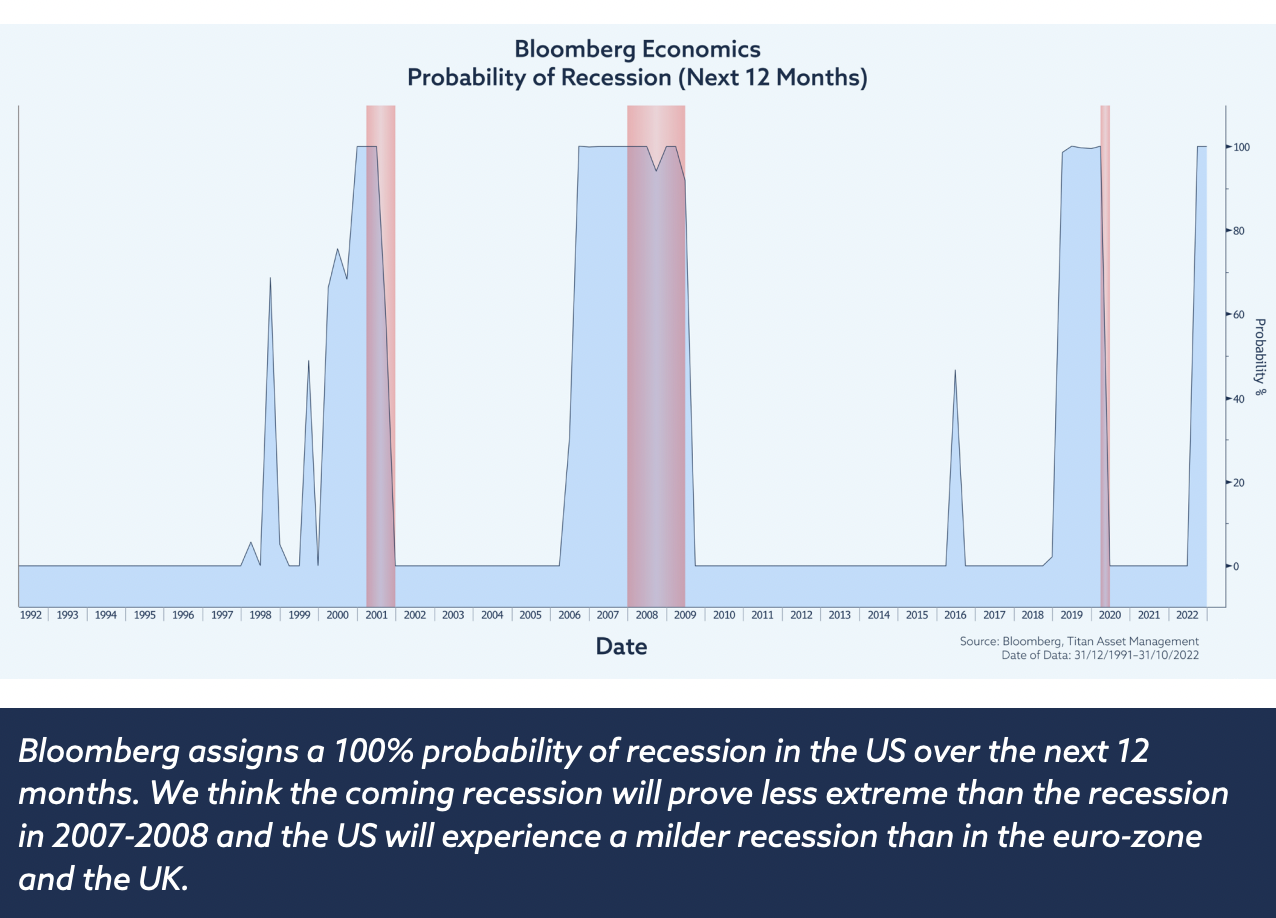

Given the magnitude of the recent relief-rally across equity markets, we think it is hard to make the case for further sustained gains. Whilst it can be difficult to forecast recessions, and the hard economic data has proven resilient thus far, we do believe a recession is likely next year given supporting anecdotal evidence from survey data, including PMIs, and our outlook for a reduction in aggregate demand. The main reason we expect demand to weaken is that the full and lagged effects of monetary tightening have yet to be felt.

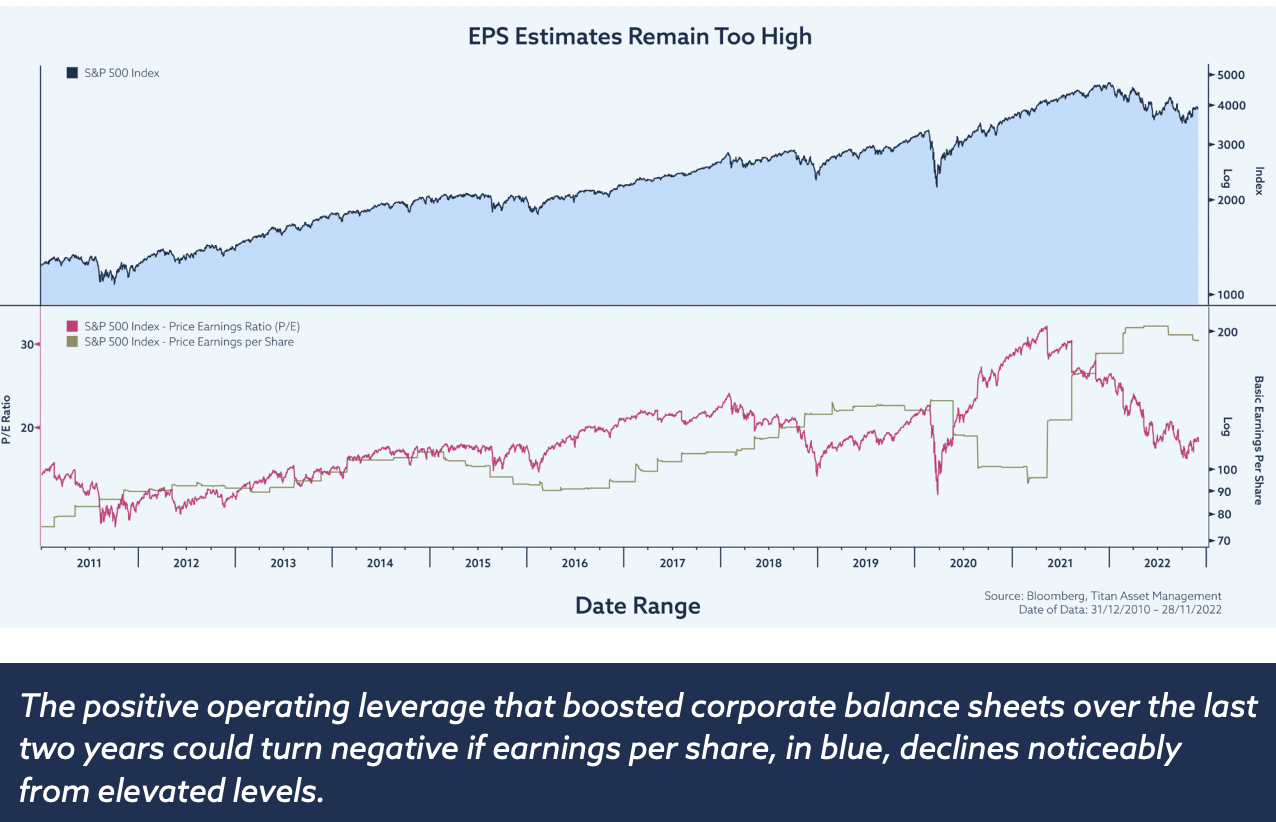

The lack of bad news in corporate earnings is a positive, but much of that growth came from energy companies which have benefited from higher oil and gas prices. At the same time there are growing signs that many households are getting squeezed and if the consumer starts to balk at what companies are charging then this could start to hit the bottom line.

The market seems to be underestimating this risk, which we think could come to the fore next earnings season in January and February. In the same way as quantitative easing and the resulting inflation led to outsized earnings power for many companies, the shift to quantitative tightening, and falling inflation, is likely to hit the bottom line.

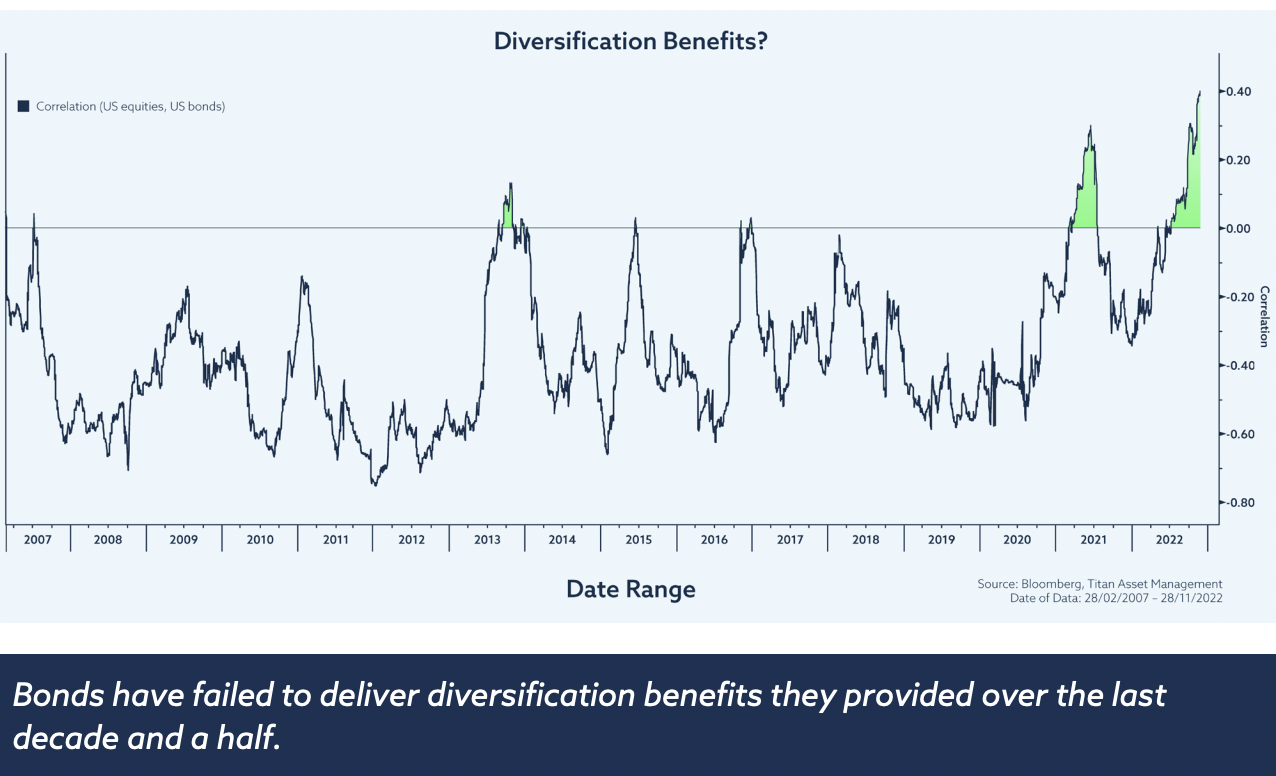

An important factor to consider over the last year, is that the traditional diversification benefits of bonds within a balanced 60/40 portfolio have deteriorated significantly. This is due to the rise in inflation and the increase in correlation between bonds and equities (both moving together). This has contributed to the larger than expected fall across the lower risk funds this year.

Looking ahead there may well come a point, given how far bond yields have backed-up, when the role of bonds in a traditional portfolio might re-establish itself. That would be consistent with both the growing recessionary narrative and potential for inflation, and interest rates, to peak and roll over in 2023.

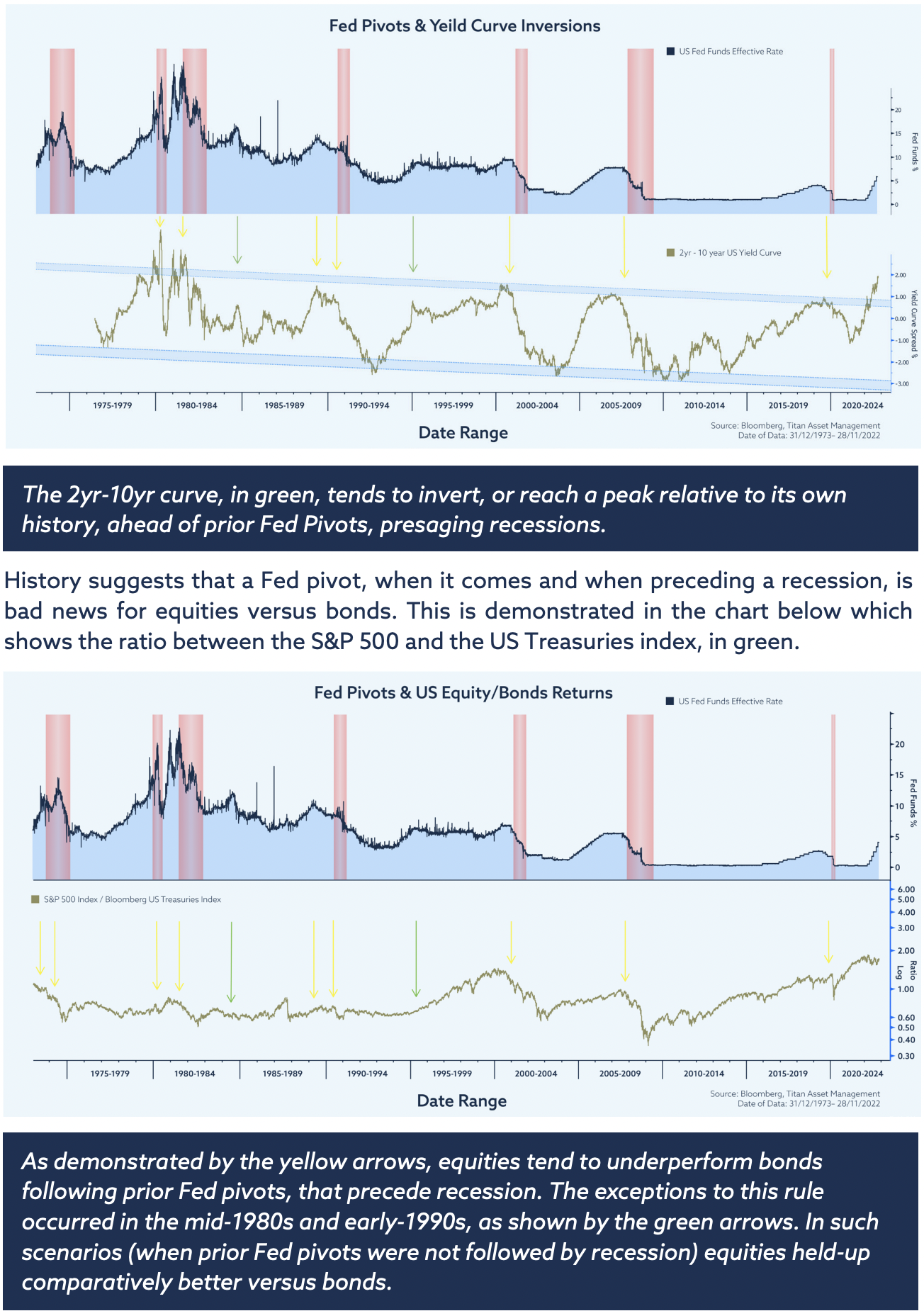

We think this will be the central theme of 2023, with the Fed funds rate peaking at around 5%, consistent with current futures pricing, before subsequently heading lower. Whilst timing this rotation will be tricky, there are a number of metrics we monitor for this purpose, such as the spread between the 2 and 10-year US Treasury yield.

This spread tends to invert, or reach a peak relative to its own history, ahead of prior Fed pivots, presaging recessions. It might take some time to get there, given central bankers remain committed to fighting inflation in the near-term, but we believe we are approaching a potential turning point later next year.

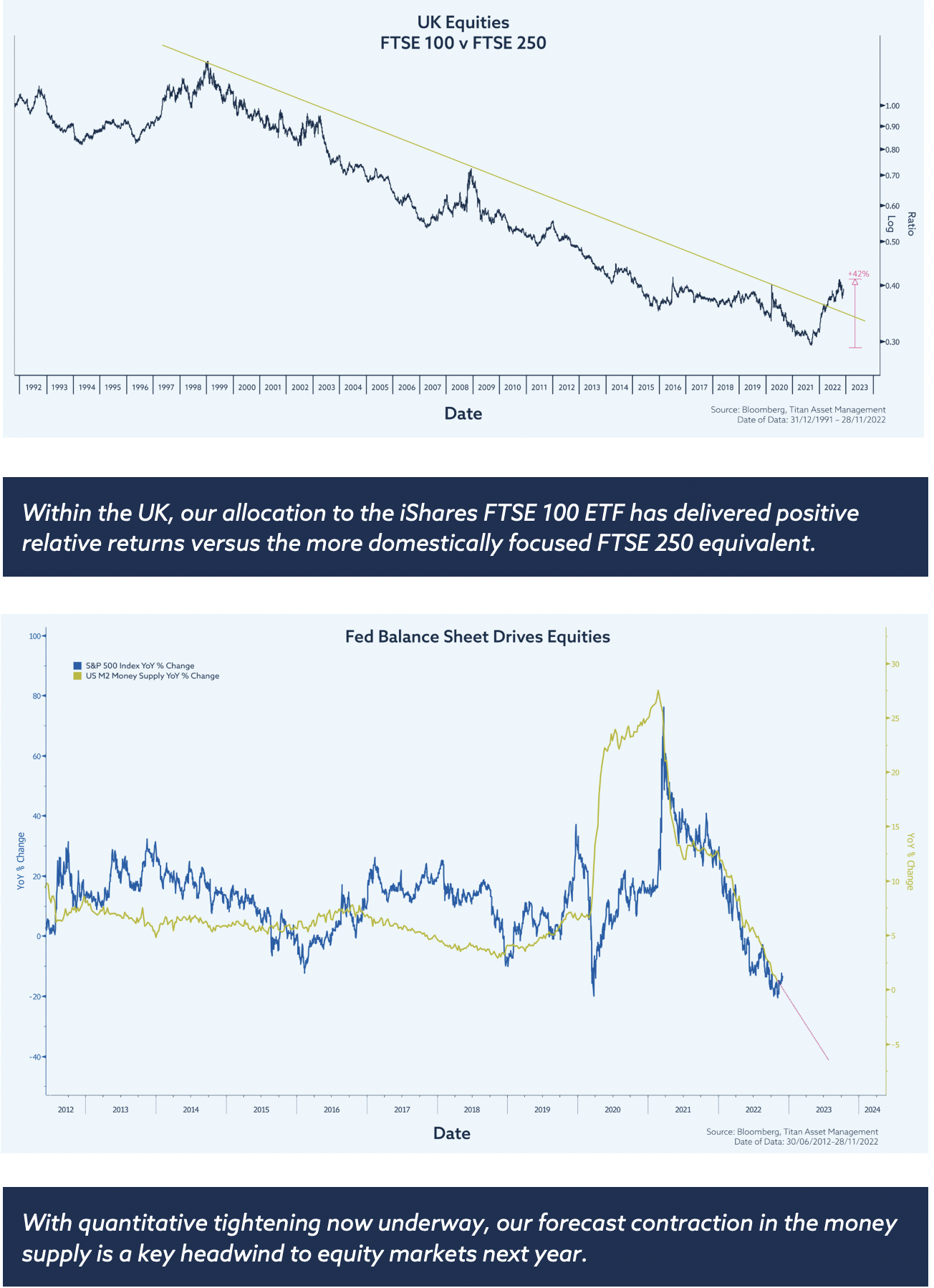

Given this macro-outlook, we remain defensively positioned across the proposition. We are more inclined to fade the recent rally, than to chase it, and we are looking to increase our exposure to bonds, and reduce equities, over time. Within equities we retain a preference for quality-focused, dividend-paying companies, minimum volatility stocks and defensive sectors, such as healthcare.

In fixed income we are similarly focused on higher quality credit, and we are looking to incrementally increase duration across government bonds next year. If the last few years have taught us anything it is that unexpected shocks can materialise out of nowhere. With that in mind we retain a pragmatic outlook, willing to adjust and adapt as required to the ever-evolving investment climate, exercising good risk management throughout.

Fixed Income

For much of the last year we have retained a preference for short-duration fixed income assets across government debt and corporate bonds. Central banks will likely continue to tighten policy until they are convinced that inflation has stabilised and started falling back towards trend. However, given our evolving market outlook, as detailed in the key themes section, we are increasingly focused on an eventual pivot in Fed policy next year, as inflation rolls-over, unemployment picks-up and recession drives asset allocators back towards safe-haven assets.

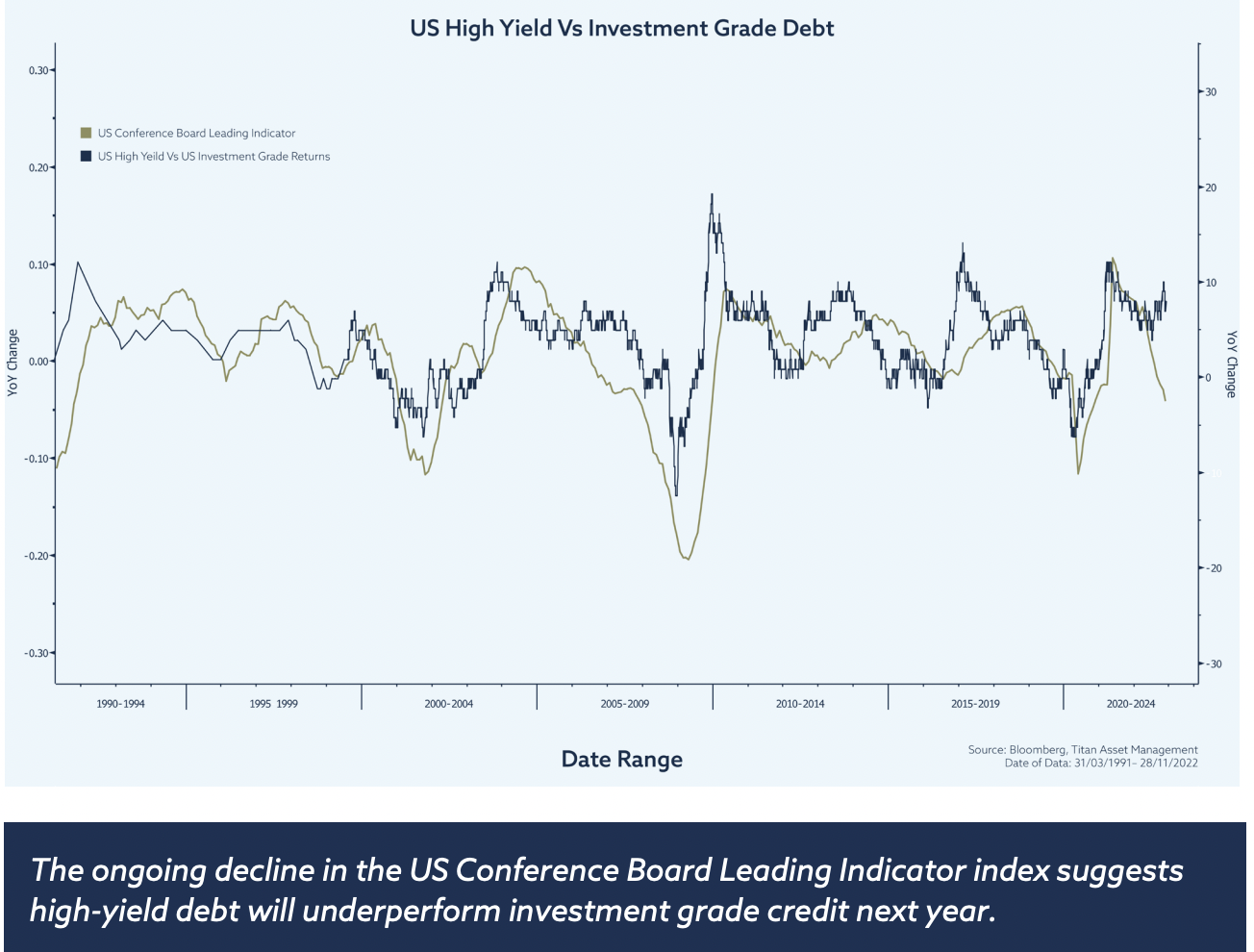

Whilst it is too early to make that call outright, we have started to slightly increase our fixed income exposure, primarily by extending our government bond duration via the belly of the curve where we see the best value. In corporates the interesting development this year is the unusual outperformance of high yield versus investment grade debt, given its shorter duration profile. We think this anomaly will give way as duration risks recede and credit risk picks-up next year against a backdrop of falling nominal GDP, free cashflow and tightening credit standards.

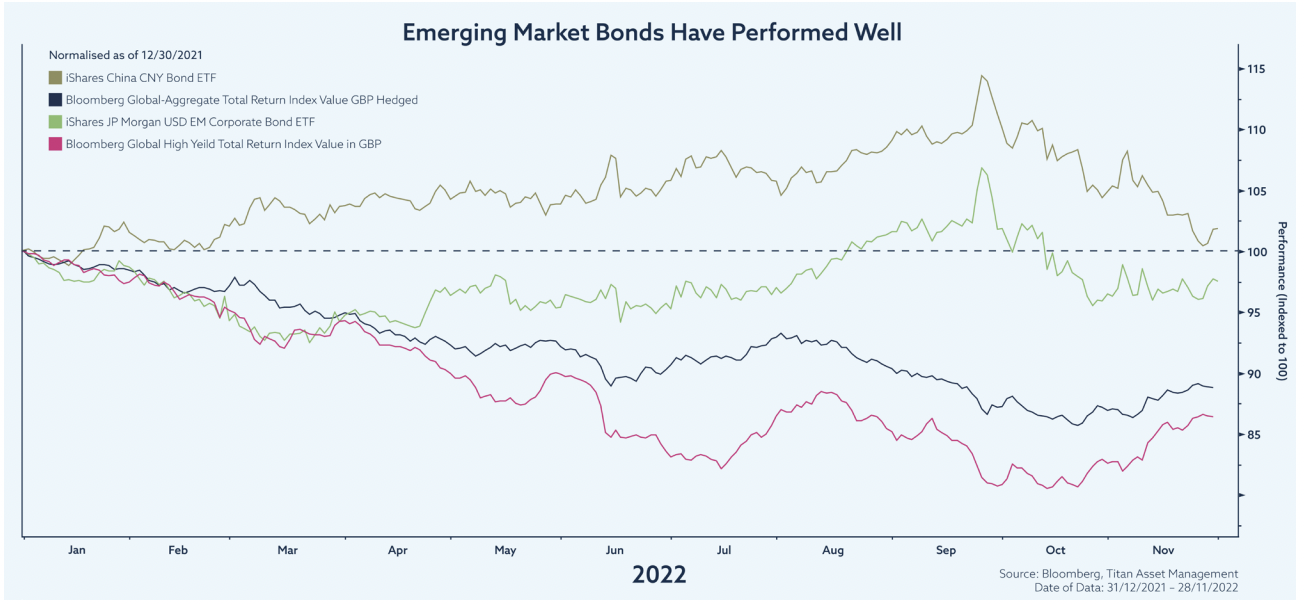

Emerging market debt has also held up better than expected. As demonstrated below, the iShares China bond ETF and the iShares JP Morgan USD EM Corporate bond ETF, which we hold in the ACUMEN Portfolios, have outperformed the generic Bloomberg Global Aggregate and High Yield indices so far this year. That said, this outperformance has reversed over the last couple of months, and we see rising headwinds in an environment of broad-based risk aversion. As such both positions remain on our watchlist.

Equities

Global equities suffered a bruising third quarter as the plethora of macroeconomic headwinds showed no signs of dissipating. Tighter financial conditions and rising yields were a major headwind as the 10-year US Treasury yield breached 4% for the first time since 2008. The MSCI World declined -6.07% in Q3 with a broad selloff across all regions. The S&P 500 hit new lows for the year with a particularly painful September where every sector was in the red, fitting for September’s reputation for historically poor returns. It marked the S&P 500’s worst year-to-date Q3 return since 2002.

We remain defensively positioned as we see further risk to the downside. The re-rating of equity multiples so far this year has been largely driven by higher rates as opposed to a decline in earnings. A key risk going forward is a deterioration in earnings that appears not to be fully priced into the market as of yet. At the headline index level, profit margins have proved resilient despite the macro headwinds, but some cracks have begun to appear.

A few individual names have grabbed the headlines recently for profit warnings; with Fedex being among the standouts who cited the macroeconomic backdrop as a major challenge resulting in slowing shipping volumes. Weakness among logistics companies has historically been a leading indicator for declining corporate margins. Our equity exposure is skewed towards companies with strong balance sheets, high profitability and low earnings volatility. While our equity outlook is cautious, we are mindful that sentiment can change quickly, and relief rallies should not come as a surprise such as the moves seen in July and more recently in October and early November.

To counter this risk, we have added some balance to our factor exposure by reopening positions in quality-focused US large cap technology stocks and a basket of clean energy companies as we are more constructive on valuations from when we took profit. The US economy looks better positioned to withstand the macroeconomic climate relative to its developed market peers due to robust consumer and corporate balance sheets. Being less entrenched with supply-side price pressures compared to Europe should also favour their equity market.

Physicals

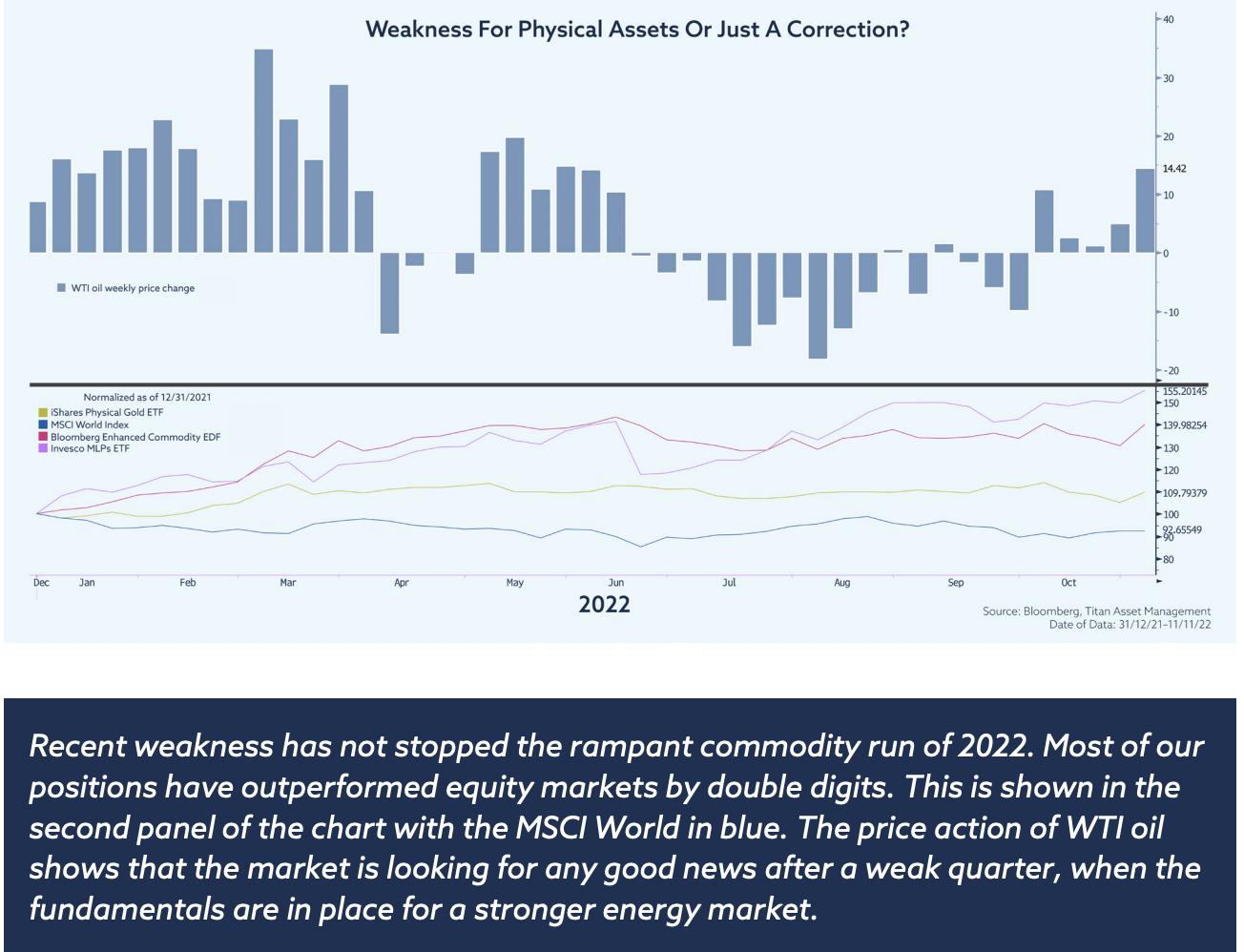

Last quarter saw demand destruction and woes of a truculently strong US dollar cause a reversal in commodity price action. Despite the ongoing war in Ukraine and persistent inflation, our conviction in the relative strength of alternative asset classes failed to manifest meaningfully in performance. However, given the volatility in equity markets, our positioning held up relatively well, with our broad basket commodity and physical gold positions only underperforming MSCI world by around 1%.

Given a 12% increase in the US dollar index, the fact that our broad-based commodity basket is still outperforming year-to-date provides support to the fundamental case for commodities in this macro-environment, despite currency and policy headwinds. A bright spot in the physicals landscape for the quarter was the performance of our position in mid-stream energy companies, held for diversification and income yield.

This position has outperformed the MSCI World by over 40% this year which has helped contribute to a stellar quarter for the ACUMEN Income Portfolio relative to its peer group. Whilst gas prices helped support our positioning as Russia continues to manipulate Nord Stream as a political weapon, weaker demand saw oil prices post their worst quarter for a year. Taking a step back however, recent moves by OPEC+, posited first in September and again now towards the end of November, make it clear that member states are more content in an environment of higher prices and so agreed plans to curb production meaningfully.

This view is compounded by the fact EU sanctions on Russian energy will only feed through meaningfully in December onwards. Whilst China continues to grapple with Covid, we believe lockdowns will continue to fade and their economic normalization will continue. Strong initial readings of Q4 Chinese demand should also play a role in providing support to commodities relative to equities.

With further equity volatility highly likely, and policy on interest rates on both sides of the Atlantic uncertain, adding diversification and alpha through physical assets continues to be an essential part of our approach to prudent risk management.

Foreign Exchange

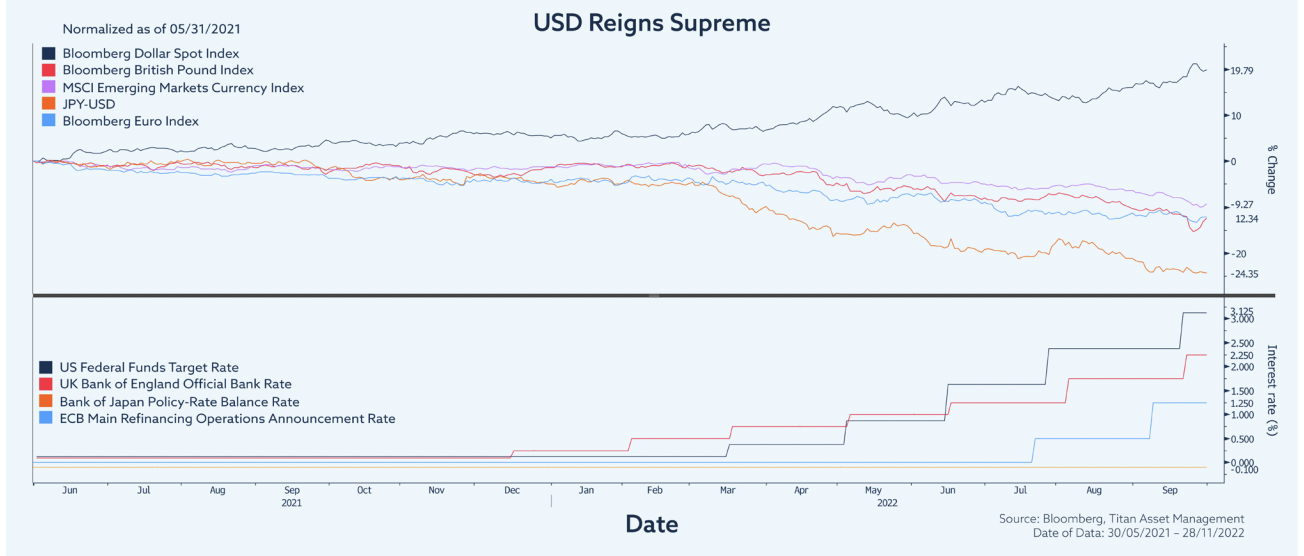

For the most part of the year global currency markets have had a torrid time. That is, of course, excluding the US dollar which continues its reign as the currency king. Dramatic fiscal moves from the new conservative government, announced by Kwasi Kwarteng, saw investors question the knock-on impact on the UK’s capital account balance and the sizeable debt pile the government would be taking on. In anticipation of, and response to, the actions laid out by the UK government gilts plummeted, spurred on by pension fund selling, sending yields soaring, whilst the UK pound tumbled to an all-time low of 1.035 against the US dollar.

The dollar has been able to remain so strong given resilient economic growth and consistent 75bps rate hikes from the US Fed in response to high inflation. It has therefore been this US dollar strength that suppressed global currencies, briefly pushing EUR/USD through parity (1.00) prior to its recent resurgence. The strong US dollar is creating real problems across the globe as the costs of imports and servicing dollar denominated debt skyrockets, whilst purchasing power diminishes: a problem some EM countries, such as Sri Lanka, have fallen victim to.

FX intervention is also back in vogue, with the Bank of Japan (BoJ) undertaking bold currency intervention measures to prevent further currency weakness. However, whilst the BoJ continues to maintain stark dovish monetary policies, currency intervention at this point seems rather futile. For now we expect wider risk-off sentiment, and declining growth prospects, to remain supportive of the dollar. Thereafter, as the likelihood of an eventual Fed pivot ratchets higher, dollar strength will start to unravel to the detriment of GBP based investors with unhedged dollar exposure.

Final Thoughts

All the above adds up to a fairly pessimistic 2023, but it is not all doom and gloom. If next year turns out better than expected it is likely to be because inflation falls at a faster pace than many currently expect, reducing the need for significant further monetary tightening.

We are seeing tentative signs of this in the October US CPI data and across various forward looking indicators. Another relative bright spot is Asia, which is expected to drive global economic growth next year versus the US and Europe where we forecast recession. There are strong underlying fundamentals driving growth in the region, which includes three of the world’s largest economies (China, India and Japan) and this strength isn’t limited to just these countries. Asian growth could help lift the global tide, bolstering export demand in Europe whilst also improving supply chains and thereby further easing the aforementioned inflationary pressures.

One factor to keep a close eye on is the growth in Chinese credit and with it the rise in the money supply. This will help support economic activity in the region and tends to lead changes in the global money supply by around 6 months. If liquidity returns to markets, which may follow a bout of risk aversion early next year, this would allow us to get more comfortable about the notion of a market-bottom from which risk assets can start to rise.

Within Asia, India looks the most exciting. GDP is forecast to expand 7% next year versus real global growth of 2.1% and with investors arguably under allocated to the region there is a strong argument for additional fund flows on the back of rising institutional demand.

Following the outbreak of the Russia-Ukraine war and mounting evidence of a great decoupling between the two biggest global players, Chimerica, India is well placed to benefit as multinational companies seek to diversify supply chains. With 30% of global manufacturing completed in China, a one-third shift towards this “China Plus One” approach represents a $1 trillion opportunity to corporate India.

Add to that a series of key structural reforms including the Production-Linked Incentive Plan, a skilled and low-cost labour force alongside a whole host of infrastructure upgrades and we see a strong and growing shift towards “Made In India”. Since the coronavirus pandemic Indian equities have outperformed broader emerging markets.

This takes relative performance to the top of its long-term range, which suggests much of the good news could already be in the price. We are watching for a technical breakout to the upside, for tangible signs of a potential new golden age of structural outperformance.

John Leiper

John Leiper is the Chief Investment Officer of Titan Asset Management and carries direct responsibility for all investments in the Centralised Investment Proposition (CIP) at the firm.